Canada Steel Market Size, Share, Trends and Report | 2025-2034

Comprehensive Analysis of Canada’s Steel Market Trends, Demand Drivers, and Forecast Growth Outlook

Canada Steel Market Outlook

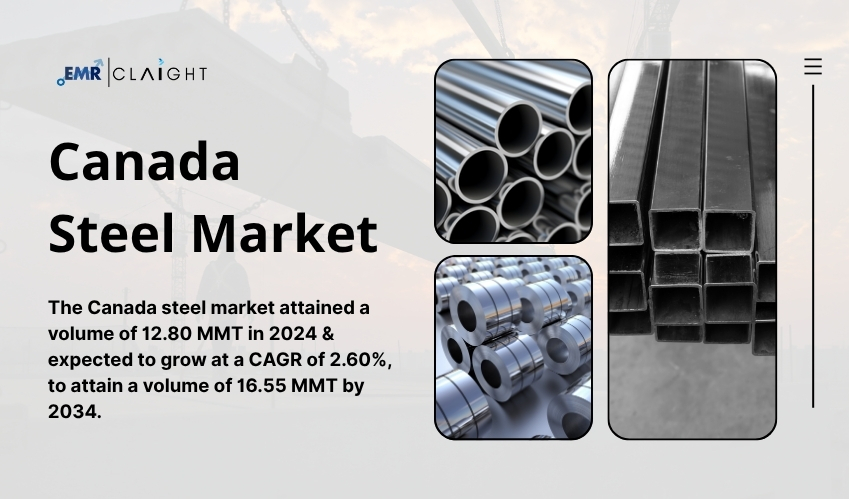

The Canada steel market reached a volume of 12.80 million metric tonnes (MMT) in 2024. Driven by increased infrastructure development, rising demand in automotive and manufacturing sectors, and growing investments in green steel technologies, the market is expected to grow at a compound annual growth rate (CAGR) of 2.60% during the forecast period of 2025 to 2034, reaching a projected volume of approximately 16.55 MMT by 2034.

Steel plays a foundational role in Canada’s economic development, supporting a wide range of industries including construction, transportation, energy, and consumer goods. The Canadian steel industry is known for its highly skilled workforce, stringent quality standards, and environmentally responsible production practices. As the country advances its decarbonisation goals and strengthens its domestic manufacturing base, the steel sector is poised for sustainable and steady growth.

Canada Steel Market Size

The size of the Canada steel market in 2024 underscores its integral role in national industrial output. At 12.80 MMT, the industry’s volume reflects robust demand across multiple end-use sectors. Public and private infrastructure projects, particularly in urban development, transportation, and energy, significantly contribute to this volume. The steady need for construction-grade long steel products like rebar, beams, and structural sections supports the market size, while demand for flat products such as hot-rolled coil, sheets, and plates is strong in automotive and appliance manufacturing.

Steel consumption in Canada is also shaped by its strategic partnerships and trade relationships, notably with the United States. The North American integrated supply chain allows Canadian producers to maintain competitive volumes while also facilitating cross-border trade. The market size is further influenced by domestic efforts to replace ageing infrastructure, expand public transit systems, and meet rising residential and commercial construction demands.

Canada Steel Market Share

The Canadian steel market is dominated by a few key players, with a significant portion of the market controlled by integrated steel producers such as Stelco Holdings Inc., Algoma Steel Group Inc., and ArcelorMittal Dofasco. These companies maintain large-scale operations and benefit from established logistics, technical expertise, and long-standing relationships with buyers in construction, manufacturing, and export markets.

By product type, flat steel products account for a substantial market share due to their extensive use in automotive, appliances, and shipbuilding industries. Long products, including bars and rods, command a strong presence in construction and infrastructure development. Stainless and specialty steels also hold niche shares, particularly in the energy sector and industrial equipment manufacturing.

Geographically, Ontario is the leading steel-producing province, home to major production facilities and industrial hubs. Quebec and Alberta also contribute significantly to market share, supported by regional manufacturing demand and resource-driven economic activity. The regional distribution of market share reflects proximity to end-users, transportation infrastructure, and port access for international trade.

Request your free report sample now and see the contents firsthand

Canada Steel Market Trends

Several trends are shaping the evolution of the Canada steel market. A notable trend is the transition toward low-carbon and green steel production. With Canada committing to ambitious net-zero emissions targets, steelmakers are investing in electric arc furnace (EAF) technology and exploring hydrogen-based production methods to reduce the carbon footprint of steel manufacturing.

Another key trend is the increasing use of recycled scrap metal in steel production. The push for sustainability, coupled with EAF adoption, is enhancing the demand for ferrous scrap, which not only reduces energy consumption but also lowers greenhouse gas emissions. The circular economy approach is gaining traction across the Canadian metals industry.

Digitisation and automation are also transforming the steel sector. The integration of smart manufacturing systems, predictive maintenance tools, and advanced process control is improving operational efficiency, product consistency, and cost competitiveness. Data-driven production strategies are helping companies respond to changing demand patterns and optimise supply chain management.

The automotive industry’s shift toward electric vehicles (EVs) is influencing steel demand and product innovation. Lightweight high-strength steel (HSS) and advanced high-strength steel (AHSS) are increasingly required for vehicle bodies and chassis, prompting Canadian producers to innovate their product portfolios.

Drivers of Growth

The Canada steel market is being driven by a combination of macroeconomic and industry-specific factors. One of the primary growth drivers is increased infrastructure spending. Federal and provincial governments are investing heavily in transportation, housing, utilities, and public buildings, all of which require significant volumes of structural steel. Programs such as the Investing in Canada Infrastructure Program (ICIP) are injecting capital into long-term development projects.

Another major driver is the resurgence of domestic manufacturing. As Canada seeks to strengthen its self-reliance in critical sectors, steel plays a pivotal role in supporting machinery, automotive, shipbuilding, and fabrication industries. The proximity to the U.S. market through the USMCA trade agreement also supports Canadian steel exports and enhances overall market demand.

The push for sustainable construction and green buildings is further elevating demand for environmentally friendly steel products. Steel’s recyclability, strength-to-weight ratio, and durability make it a preferred material in LEED-certified and low-carbon construction projects.

Growing investments in renewable energy, including wind farms and solar energy infrastructure, are also contributing to steel consumption, particularly for structural frameworks, turbine towers, and transmission supports.

Canada Steel Industry Analysis

The Canadian steel industry is capital-intensive and technologically advanced, with a strong emphasis on environmental stewardship and worker safety. The sector benefits from a stable regulatory framework, access to raw materials, and an educated workforce. Canada’s steel production is characterised by high energy efficiency, with many facilities already adopting low-emission processes.

Consolidation in the industry has led to a more streamlined competitive landscape, allowing for focused capital investment and innovation. However, the industry also faces pressure from global overcapacity, particularly from low-cost imports. Trade remedies and anti-dumping measures play an essential role in protecting the domestic market.

The Canadian Steel Producers Association (CSPA) and other trade bodies actively collaborate with the government to promote fair trade, infrastructure development, and environmental innovation. The industry’s ability to respond to evolving consumer expectations and regulatory requirements has made it a resilient pillar of Canada’s industrial economy.

Canada Steel Market Segmentation

The market can be divided based on product, type, end use and region.

Market Breakup by Product

- Flat Steel

- Long Steel

Market Breakup by Type

- Carbon Steel

- Alloy Steel

- Stainless Steel

- Tool Steel

Market Breakup by End Use

- Construction

- Mechanical Engineering

- Automotive

- Domestic Appliances

- Metalware

- Agricultural

- Others

Market Breakup by Region

- British Columbia

- Alberta

- The Prairies

- Central Canada

- Atlantic Canada

Competitive Landscape

Some of the major players explored in the report by Expert Market Research are as follows:

- Algoma Steel Inc.

- ArcelorMittal Dofasco

- Stelco Inc.

- Gerdau S/A

- Rolled Alloys

- Canam Group Inc.

- LMS Reinforcing Steel Group

- Walters Inc.

- Others

Challenges and Opportunities

Despite its strengths, the Canada steel market faces several challenges. One of the most pressing is global market volatility. Fluctuations in raw material prices, particularly iron ore and coking coal, can impact production costs and profit margins. Geopolitical tensions and trade disruptions also pose risks to export stability.

Environmental regulations, while necessary, present both financial and technological challenges for steelmakers. Transitioning to low-carbon technologies requires significant investment, and the pace of innovation must align with policy timelines and market expectations.

Labour shortages and rising operational costs in energy and logistics are additional challenges affecting competitiveness. Moreover, competition from subsidised foreign steel threatens the market position of Canadian producers.

However, these challenges are accompanied by compelling opportunities. The transition to green steel production opens new avenues for technological leadership and premium product offerings. Canada’s commitment to decarbonisation and clean energy provides a supportive policy environment for sustainable manufacturing.

The adoption of digital technologies offers opportunities to improve productivity, reduce downtime, and optimise resource use. Expansion into value-added products such as coated steels, specialty alloys, and prefabricated components can help producers differentiate themselves and capture higher margins.

Furthermore, participation in strategic infrastructure projects, such as EV charging networks, rail expansions, and renewable energy installations, offers sustained long-term demand for steel products.

Canada Steel Market Forecast

The Canada steel market is poised for steady growth over the next decade. From a volume of 12.80 MMT in 2024, the market is expected to reach 16.55 MMT by 2034, growing at a CAGR of 2.60% during the forecast period. This expansion will be supported by infrastructure development, rising demand for sustainable materials, and the revival of domestic manufacturing.

As environmental concerns reshape the global metals industry, Canada’s steel sector is well-positioned to lead through innovation, responsible sourcing, and strategic investment. Companies that align with green building standards, digital transformation, and customer-centric supply chains will be best positioned to capitalise on emerging opportunities.

With a strong foundation and a forward-looking vision, the Canada steel market is set to play a vital role in the country’s economic, environmental, and industrial transformation through 2034 and beyond.

Media Contact:

Company Name: Claight Corporation

Email: sales@expertmarketresearch.com

Toll Free Number: +1-415-325-5166 | +44-702-402-5790

Address: 30 North Gould Street, Sheridan, WY 82801, USA

Website: http://www.expertmarketresearch.com